2026 年上半年中国新增 67 家独角兽:AI、机器人、DeepSeek 与新科技周期

本文梳理 2026 年上半年中国新增 67 家独角兽企业,覆盖行业分布、城市集群、估值梯队、企业年龄、DeepSeek 估值,以及 AI 和机器人赛道的崛起。

China’s 67 New Unicorns in H1 2026: AI and Robotics Drive a New Growth Cycle

Introduction

China added 67 newly listed unicorn companies in the first half of 2026, according to ITjuzi data cited in the original report. That works out to roughly one new unicorn every three days and marks the strongest half-year increase in nearly five years.

The composition of this new group is more important than the headline count. Artificial intelligence and robotics account for more than half of the companies, while semiconductor, quantum computing, intelligent vehicles, biotechnology, and other hard-technology fields make up much of the remainder.

DeepSeek is the largest company in the new cohort by estimated valuation. Its presence also changes the overall averages: most of the 67 companies remain close to the standard US$1 billion unicorn threshold, while a small number of highly valued AI companies contribute a disproportionate share of the group’s total value.

This article reorganizes the original Chinese report into a publication-ready English version. It preserves the same analytical sequence: overall numbers, historical comparison, sector distribution, city distribution, valuation structure, time to unicorn status, and the outlook for the second half of the year.

China’s Unicorn Market at a Glance

As of July 1, 2026, ITjuzi’s database counted 517 active Chinese unicorn companies with an estimated combined valuation of approximately US$2.39 trillion.

The broader market still has a clear pyramid structure:

- 57.3% of companies are valued between US$1 billion and US$2 billion.

- 30.8% fall between US$2 billion and US$5 billion.

- 62 companies, or around 12%, are valued above US$5 billion.

- Only five companies are valued above US$50 billion.

The five companies at the top of the full database are ByteDance, Ant Group, SHEIN, DeepSeek, and Xiaohongshu. Together, they contribute roughly 36% of the total valuation recorded in the database.

Geographically, Beijing, Shanghai, and Shenzhen remain the largest unicorn centers. The three cities account for 301 of the 517 companies, or 58.2% of the national total. Hangzhou ranks behind them by company count but contributes an unusually large share of valuation because DeepSeek is headquartered there.

At the industry level, advanced manufacturing leads the full database, followed by artificial intelligence and healthcare. Robotics has moved ahead of e-commerce and retail, reflecting the continued shift from consumer-internet businesses toward AI infrastructure, embodied intelligence, advanced components, and industrial technology.

01. Sixty-Seven New Unicorns, Led by DeepSeek

In the first half of 2026, 67 Chinese companies newly entered the unicorn category. Their combined estimated valuation reached US$182.9 billion.

| Metric | H1 2026 result |

|---|---|

| Newly listed unicorns | 67 |

| Combined valuation | US$182.9 billion |

| Average valuation | US$2.73 billion |

| Median valuation | US$1.409 billion |

| Highest valuation | DeepSeek, about US$61.538 billion |

The average valuation of the new cohort is about half the average across all Chinese unicorns in the database. The median is also slightly below the full-market median.

This suggests that most of the newly listed companies have only recently crossed the US$1 billion threshold. They are still in an earlier growth stage than many established unicorns.

At the same time, the average is pulled upward by a small number of outliers. DeepSeek alone represents roughly one-third of the total valuation of the 67-company cohort. Kling AI, estimated at US$18 billion in the source data, is another unusually large company compared with the rest of the group.

The result is a market with two very different layers:

- A broad base of young companies valued between US$1 billion and US$2 billion.

- A small number of AI leaders receiving much larger valuation premiums.

02. Historical Comparison: A New Growth Cycle Begins

The first half of 2026 is the second-strongest half-year period for newly listed Chinese unicorns in the dataset.

The highest point remains the second half of 2021, when 76 companies entered the ranking. H1 2026 follows with 67, ahead of H1 2021, H2 2020, H2 2022, and H1 2022.

Two peaks with different foundations

The 2021–2022 expansion was distributed across several industries. New energy, biopharmaceuticals, consumer internet platforms, automotive supply chains, and digital services all contributed to the increase.

The 2026 rebound is much more concentrated.

Of the 67 new unicorns:

- 19 are classified as robotics companies.

- 17 are classified as artificial-intelligence companies.

- Together, those two sectors account for 36 companies, or more than 53% of the cohort.

This is not simply another broad startup-financing cycle. It is a technology-specific wave centered on large models, generative AI, AI infrastructure, humanoid robotics, embodied intelligence, intelligent hardware, and key components.

The difference matters because concentrated cycles can move faster. Technical breakthroughs, large-company spinouts, experienced founding teams, and investor consensus can all push valuations upward within a short period.

They can also create greater risk. When many investors converge on the same sectors, crowded markets and valuation inflation become more likely.

03. Sector Distribution: Robotics and AI Form the Two Main Engines

The 67 companies span ten primary sectors. Robotics ranks first by company count, while artificial intelligence contributes by far the largest combined valuation.

| Sector | Companies | Share | Combined valuation | Average valuation |

|---|---|---|---|---|

| Robotics | 19 | 28.4% | US$34.233B | US$1.802B |

| Artificial intelligence | 17 | 25.4% | US$104.715B | US$6.160B |

| Semiconductors | 8 | 11.9% | US$10.406B | US$1.301B |

| Frontier technology | 7 | 10.4% | US$11.231B | US$1.604B |

| Intelligent vehicles | 6 | 9.0% | US$7.455B | US$1.242B |

| Biotechnology and pharmaceuticals | 5 | 7.5% | US$7.592B | US$1.518B |

| Aerospace | 2 | 3.0% | US$2.969B | US$1.485B |

| Enterprise services | 1 | 1.5% | US$1.077B | US$1.077B |

| New energy | 1 | 1.5% | US$1.870B | US$1.870B |

| Advanced manufacturing | 1 | 1.5% | US$1.352B | US$1.352B |

Robotics expands across the full value chain

The 19 robotics companies are not limited to humanoid-robot manufacturers. The group includes:

- Complete humanoid-robot platforms

- Dexterous hands and other core components

- Embodied-intelligence software

- Robot control and perception systems

- Industrial and logistics robots

- Robot leasing and commercial-service models

Eight companies are identified with the humanoid-robot direction. Variable Robotics, AI² Robotics, and Spirit AI are among the higher-valued names in this group.

The cohort also shows the influence of technology spinouts. AGILINK emerged from a dexterous-hand team associated with AgiBot, while D-Robotics grew from Horizon Robotics’ AIoT business. These companies begin with existing technical assets, engineering teams, and industry relationships, making it easier to raise capital quickly.

AI valuations are highly concentrated

The 17 artificial-intelligence companies have a combined valuation of about US$104.715 billion. DeepSeek accounts for close to 59% of that amount.

Removing DeepSeek leaves the other 16 AI companies with a combined valuation of approximately US$43.2 billion, or an average of around US$2.7 billion each.

The sector covers several directions:

- Foundation models

- AI agents and productivity systems

- Multimodal image and video generation

- AI chips and compute infrastructure

- Model-serving platforms

- AI-assisted drug discovery

- Vertical industry AI

Kling AI is the second-largest AI company in the cohort by valuation. AI infrastructure also remains active, with companies such as Sunrise, Iluvatar-style chip and compute ventures, SiliconFlow, and Infinigence-type infrastructure providers attracting continued investment.

Semiconductors and frontier technology remain important

Eight newly listed semiconductor unicorns cover automotive chips, communications chips, AI accelerators, autonomous-driving processors, advanced packaging, and semiconductor equipment.

The frontier-technology group includes four quantum-computing companies: Origin Quantum, SpinQ, TuringQ, and QBoson. Their presence suggests that quantum technology in China is moving from laboratory research toward early industrial deployment and commercial financing.

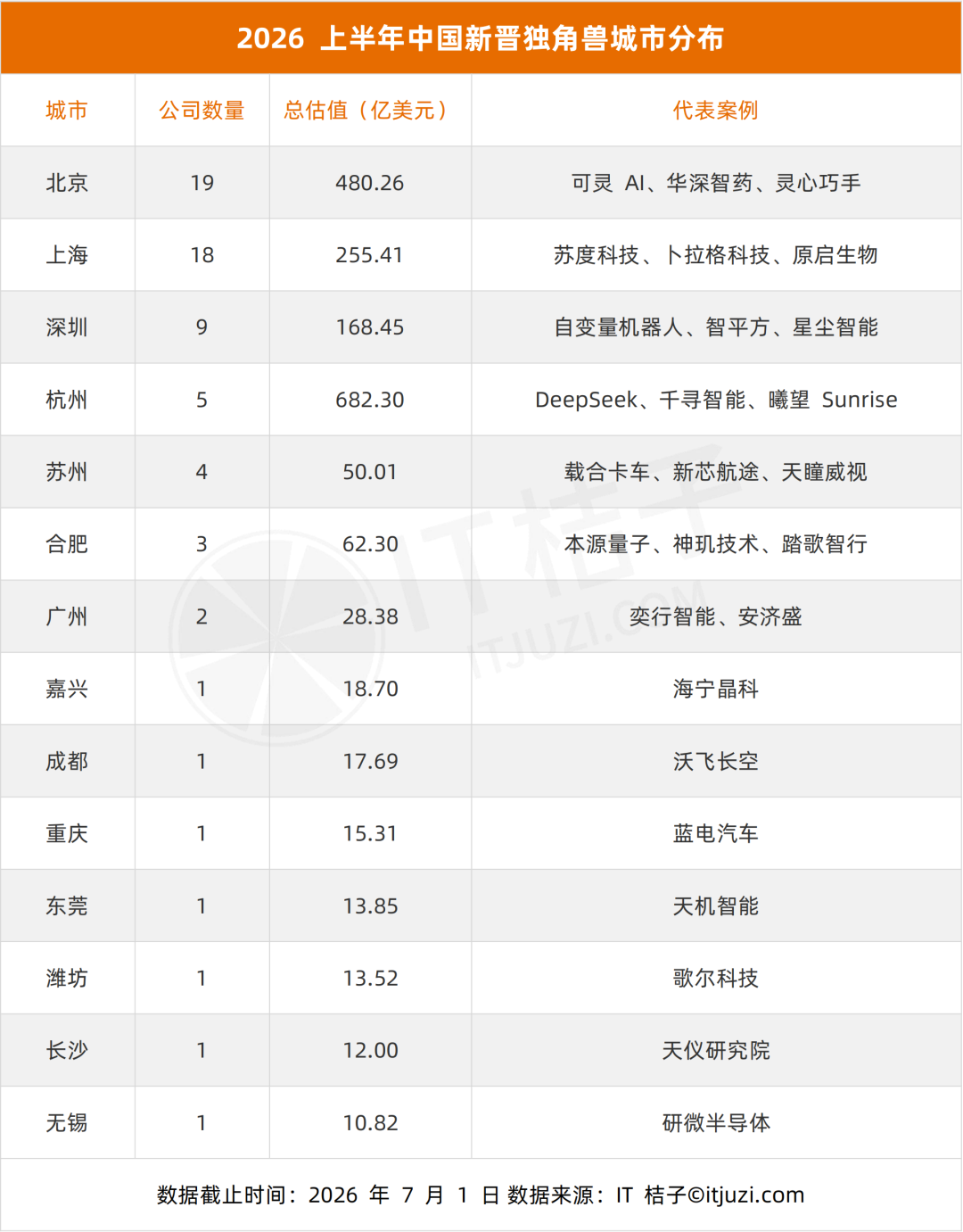

04. City Distribution: Beijing, Shanghai, Shenzhen, and Hangzhou Dominate

The 67 companies are distributed across 14 cities, but the concentration is high.

Beijing, Shanghai, Shenzhen, and Hangzhou together account for 51 companies, or 76.1% of the total.

| City | New unicorns | Combined valuation | Representative companies |

|---|---|---|---|

| Beijing | 19 | US$48.026B | Kling AI, Hasten Biopharma, Spirit AI |

| Shanghai | 18 | US$25.541B | Sudo Technology, PlugAI, Oricell |

| Shenzhen | 9 | US$16.845B | Variable Robotics, AI² Robotics, Stardust Intelligence |

| Hangzhou | 5 | US$68.230B | DeepSeek, Spirit AI, Sunrise |

| Suzhou | 4 | US$5.001B | Zaihe Truck, Xincheng Hangtu, Tianmou Vision |

| Hefei | 3 | US$6.230B | Origin Quantum, Shenji Technology, Tage IDriver |

| Guangzhou | 2 | US$2.838B | Uisee, Anji Sheng |

| Jiaxing | 1 | US$1.870B | Haining Jingke |

| Chengdu | 1 | US$1.769B | Volant Aerotech |

| Chongqing | 1 | US$1.531B | Deepal Automobile |

| Dongguan | 1 | US$1.385B | Tianji Intelligent |

| Weifang | 1 | US$1.352B | Goertek Technology |

| Changsha | 1 | US$1.200B | Tianyi Research Institute |

| Wuxi | 1 | US$1.082B | Yanwei Semiconductor |

Beijing and Shanghai lead by company count

Beijing ranks first with 19 companies, while Shanghai follows closely with 18.

Beijing’s combined valuation is substantially higher because of large AI companies such as Kling AI and several well-funded AI and pharmaceutical ventures. Its strongest areas are foundation models, generative AI, embodied-intelligence software, and AI-enabled drug development.

Shanghai has a more balanced distribution across AI, semiconductors, biotechnology, intelligent vehicles, and advanced industrial technology.

Hangzhou leads by valuation

Hangzhou has only five newly listed unicorns, yet its total valuation is higher than that of Beijing and Shanghai. DeepSeek is the main reason.

This illustrates the limits of using total valuation alone to compare startup ecosystems. One exceptional company can change a city’s ranking dramatically even when the city has fewer companies overall.

Shenzhen is becoming a humanoid-robotics center

Six of Shenzhen’s nine new unicorns are classified as robotics companies. The city combines electronics manufacturing, supply-chain depth, hardware engineering, industrial design, and access to component suppliers.

Those conditions make Shenzhen especially suitable for embodied-intelligence companies that must move from prototypes to physical products.

Regional specialization is becoming clearer

Other cities show narrower but recognizable strengths:

- Hefei’s three companies are all in hard technology, including quantum computing and autonomous-driving chips.

- Three of Suzhou’s four companies are related to intelligent vehicles.

- Beijing is strongest in AI software and embodied-intelligence platforms.

- Shanghai has a more diversified mix of AI, chips, pharmaceuticals, and industrial businesses.

The pattern suggests that the next generation of unicorns will depend heavily on local talent clusters, laboratories, supply chains, industrial customers, and financing networks.

05. Valuation Structure: A Broad Base and Very Few Super Unicorns

The valuation distribution of the new cohort forms a steep pyramid.

| Valuation range | Companies | Share |

|---|---|---|

| US$1B–US$2B | 52 | 77.6% |

| US$2B–US$5B | 13 | 19.4% |

| US$5B–US$10B | 0 | 0% |

| Above US$10B | 2 | 3.0% |

More than three-quarters of the companies are valued between US$1 billion and US$2 billion. Most have therefore only recently passed the standard unicorn threshold.

Thirteen companies fall between US$2 billion and US$5 billion. This group includes businesses that have generally demonstrated stronger financing momentum, technical differentiation, or early commercial validation.

The most unusual feature is the complete absence of companies in the US$5 billion to US$10 billion range.

Instead, the distribution jumps directly to two companies above US$10 billion:

- DeepSeek at approximately US$61.538 billion

- Kling AI at approximately US$18 billion

This gap shows how sharply investors distinguish leading foundation-model or generative-AI companies from the wider startup market. In those categories, technical leadership and expectations of platform-scale growth can produce valuation premiums far beyond those of ordinary unicorns.

It also creates greater uncertainty. Private-company valuations can move quickly if growth, product adoption, financing conditions, or competitive expectations change.

06. Time to Unicorn Status: Fast and Slow Paths Diverge

The 67 companies show two very different development patterns.

Companies founded in 2023 form the largest group, with 14 companies. Another ten were founded in 2022, and eight in 2021. Together, companies established during those three years account for nearly half the cohort.

The timing closely follows the acceleration of generative AI and embodied intelligence after 2023.

The average time from founding to unicorn status was 4.7 years, while the median was 3.7 years.

- 34.3% reached unicorn status within three years.

- 67.2% reached it within five years.

- Twelve companies took more than eight years.

The fastest companies are concentrated in AI and robotics

The fastest five companies reached unicorn status within six months.

| Rank | Company | Time to unicorn | Sector |

|---|---|---|---|

| 1 | PlugAI | 0.1 years | Artificial intelligence |

| 2 | Kunlunxing Robotics | 0.3 years | Robotics |

| 3 | AGILINK | 0.4 years | Robotics |

| 4 | Zhiyan Huisheng | 0.4 years | Artificial intelligence |

| 5 | Qingtianzu | 0.5 years | Robotics |

These companies often began with one or more advantages:

- Founders with strong academic or industry reputations

- Teams spun out from large technology companies

- Existing patents, models, hardware designs, or customer relationships

- Immediate access to investors and strategic partners

- Entry into sectors receiving intense market attention

PlugAI, for example, was founded by former Alibaba Qwen model leader Lin Junyang and entered the database as a unicorn shortly after establishment. AGILINK originated from an experienced robotics team. Sunrise emerged from a large AI-chip organization. Zhiyan Huisheng was founded by an academic specialist and reached unicorn status within months.

These cases are sometimes described as “born unicorns.” Their early valuations are based less on years of financial performance and more on team quality, technical assets, strategic importance, and expected future growth.

Hard-technology companies take longer

The slowest path appears in semiconductor, biotechnology, advanced manufacturing, and other capital-intensive fields.

Examples in the report include companies that took 11 to 14 years to reach unicorn status. Their products require longer research cycles, engineering validation, manufacturing readiness, regulatory approval, and customer adoption.

This produces two parallel startup economies:

- Fast AI and robotics companies, where experienced teams and market expectations can generate high valuations quickly.

- Slow hard-technology companies, where value accumulates through long-term research, engineering, manufacturing, and certification.

Both paths are likely to remain part of China’s technology market.

07. Trends and Outlook

The 67 new unicorns indicate that China has entered another startup-growth cycle, but this cycle looks different from the one seen in 2021 and 2022.

The growth engine is more concentrated

The previous peak included new energy, healthcare, consumer internet, and multiple other industries. The 2026 cohort depends much more heavily on AI and robotics.

That concentration reflects strong investor agreement about the next major technology platforms. It also means that the market is more exposed to competition, duplicated products, weak commercialization, and valuation corrections within those two sectors.

Companies are reaching unicorn status faster

More than one-third of the cohort crossed the threshold within three years. Many are spinouts or companies founded by high-profile researchers and executives.

This can be a positive sign of efficient technology transfer. Experienced teams are converting research, models, chip designs, and robotics systems into independent businesses more quickly.

However, fast valuation growth may arrive before product-market fit, stable revenue, or scalable delivery. The key question is whether these companies can meet commercial expectations within the next one or two years.

Hard technology is becoming more visible

Semiconductors, quantum computing, aerospace, nuclear-fusion-related technology, biotechnology, and advanced manufacturing all appear in the new cohort.

These businesses usually grow more slowly than software companies, but they are increasingly important to supply-chain resilience, industrial upgrading, and technology independence.

The contrast between rapid AI valuations and long-cycle industrial innovation will continue to shape financing strategies.

City concentration is increasing

The four leading cities account for 76.1% of new unicorns, compared with 58.2% of all active unicorns in the database.

New technology companies depend on dense networks of talent, research institutions, suppliers, customers, and investors. As a result, Beijing, Shanghai, Shenzhen, and Hangzhou may continue to absorb a larger share of high-growth startups.

Cities outside those clusters can still build strong positions, but they may need to focus on specialized industries where they have research or manufacturing advantages.

AI and robotics are likely to remain the main sources of new unicorns

In the second half of 2026, embodied intelligence is expected to move further from laboratory demonstrations toward pilot production and commercial deployment.

That could bring more robot manufacturers, dexterous-hand developers, perception providers, motion-control companies, and component suppliers above the US$1 billion threshold.

Semiconductor and quantum-computing companies will continue to benefit from long-term domestic technology demand, although their financing pace may be more sensitive to policy and capital-market conditions.

The biggest test will be commercialization. Lightning-fast unicorns now need to prove that technical reputation and investor enthusiasm can become repeatable revenue, defensible products, and sustainable operations.

Appendix: Complete List of the 67 Newly Listed Unicorns

The original report presented the full list as a single promotional image containing a QR code. To preserve the information without reproducing the QR code, the company names are listed below as text.

| No. | Company | No. | Company | No. | Company |

|---|---|---|---|---|---|

| 1 | DeepSeek | 24 | Sunrise (曦望 Sunrise) | 46 | CIX Technology (此芯科技) |

| 2 | Kling AI (可灵 AI) | 25 | Jiyu Pharma (济煜医药) | 47 | Xincheng Hangtu (新芯航途) |

| 3 | Hasten Biopharma (华深智药) | 26 | SiliconFlow (硅基流动) | 48 | RayNeo (雷鸟创新) |

| 4 | Origin Quantum (本源量子) | 27 | Zaihe Truck (载合卡车) | 49 | Tianyi Research Institute (天仪研究院) |

| 5 | Variable Robotics (自变量机器人) | 28 | Yixing Intelligence (奕行智能) | 50 | Suanmiao Technology (算苗科技) |

| 6 | AI² Robotics (智平方) | 29 | X-World Intelligence (跨维智能) | 51 | Wujie Power (无界动力) |

| 7 | Spirit AI (千寻智能) | 30 | Xingxuan Technology (星旋科技) | 52 | LimX Dynamics (逐际动力) |

| 8 | Linker Hand / Lingxin Qiaoshou (灵心巧手) | 31 | AGILINK (临界点 AGILINK) | 53 | Zhijian Power (至简动力) |

| 9 | AgiBot World / Jiyue Shijie (极佳视界) | 32 | Shenji Technology (神玑技术) | 54 | SenseTime Healthcare (商汤医疗) |

| 10 | Sudo Technology (苏度科技) | 33 | Deepal Automobile (蓝电汽车) | 55 | Tianmou Vision (天瞳威视) |

| 11 | PlugAI (卜拉格科技) | 34 | Stream Computing / Jiliu Technology (基流科技) | 56 | Tage IDriver (踏歌智行) |

| 12 | Lightwheel (光轮智能) | 35 | Xinsi Semiconductor (星思半导体) | 57 | Yingchuang Huizhi (英创汇智) |

| 13 | LiblibAI | 36 | Kunlunxing Robotics (昆仑行机器人) | 58 | Yanwei Semiconductor (研微半导体) |

| 14 | Aishi Technology (爱诗科技) | 37 | Lingchu Intelligence (灵初智能) | 59 | Zero One Auto (零一汽车) |

| 15 | Oricell (原启生物) | 38 | Tianji Intelligent (天机智能) | 60 | Black Lake Technologies (黑湖科技) |

| 16 | Haining Jingke (海宁晶科) | 39 | Shengshu Technology (生数科技) | 61 | CloudMinds ChipLink (云脉芯联) |

| 17 | TARS Robotics / Tashi Zhihang (它石智航) | 40 | TuringQ (图灵量子) | 62 | Xinghuan Fusion Energy (星环聚能) |

| 18 | Stardust Intelligence (星尘智能) | 41 | Goertek Technology (歌尔科技) | 63 | Qingtianzu (擎天租) |

| 19 | D-Robotics (地瓜机器人) | 42 | Anji Sheng (安济盛) | 64 | Infinigence AI (无问芯穹) |

| 20 | Volant Aerotech (沃飞长空) | 43 | QBoson (玻色量子) | 65 | neueHCT / Zhijia Dalu (智驾大陆) |

| 21 | Calterah (加特兰) | 44 | Booster Robotics (加速进化) | 66 | VAST |

| 22 | Deep Intelligent Pharma (深度智耀) | 45 | BrainCo (强脑科技) | 67 | Zhiyan Huisheng (智衍慧生) |

| 23 | PaXini Tech (帕西尼) |

FAQ

What is a unicorn company?

A unicorn is a privately held startup valued at US$1 billion or more. The valuation is generally based on private financing transactions and investor expectations rather than a continuously traded public-market price.

How many new unicorns did China add in the first half of 2026?

The ITjuzi data cited in the report lists 67 newly recognized unicorns in H1 2026. Their combined estimated valuation was US$182.9 billion.

Which company had the highest valuation in the new cohort?

DeepSeek had the highest estimated valuation at approximately US$61.538 billion. It contributed a large share of both the AI sector’s valuation and the total value of all 67 companies.

Which industries created the most new Chinese unicorns?

Robotics ranked first with 19 companies, followed by artificial intelligence with 17. Together, the two sectors represented more than 53% of all newly listed unicorns.

Which Chinese city added the most unicorns?

Beijing added 19, narrowly ahead of Shanghai with 18. Hangzhou had fewer companies but the highest combined valuation because of DeepSeek.

Why is Shenzhen important for humanoid robotics?

Six of Shenzhen’s nine new unicorns were robotics companies. Its deep electronics supply chain, manufacturing capacity, hardware talent, and component ecosystem make it well suited to embodied-intelligence and humanoid-robot startups.

Why did some companies become unicorns within months?

The fastest companies were often founded by established researchers or executives, or spun out of mature technology teams. Existing intellectual property, technical talent, investor networks, and market demand allowed them to raise large financing rounds very quickly.

Are private unicorn valuations reliable?

They are useful indicators, but they are not the same as audited market capitalizations. Private valuations may be based on limited financing transactions and can change when market conditions, revenue expectations, or investor sentiment shift.

Related Tools

- ITjuzi: A Chinese database for startups, venture-capital firms, financing events, and private-market research.

- Crunchbase: A global platform for researching private companies, founders, investors, and funding rounds.

- Dealroom: A startup and innovation intelligence platform covering companies, ecosystems, and venture activity.

- CB Insights: A market-intelligence platform for tracking private technology companies and emerging industries.

- PitchBook: A professional data platform for private capital, venture investment, M&A, and company valuations.

Related Links

- ITjuzi About Us: Background on the data provider behind the report.

- SCMP: China Records Its Strongest Unicorn Growth in Five Years: Independent reporting on the H1 2026 AI- and robotics-led rebound.

- Xinhua: China’s Unicorn Company Scale: Coverage of the 2026 China Unicorn Companies Development Report.

- Beijing Government: Beijing’s Unicorn Ecosystem: Official information on Beijing’s position in China’s unicorn market.

- DeepSeek Official Website: Official information and access to DeepSeek’s models and products.

- Kling AI Official Website: Official platform for Kling’s generative video and image models.

Summary

China’s 67 newly listed unicorns in H1 2026 represent the strongest half-year expansion since the 2021 peak. Unlike the earlier cycle, this rebound is highly concentrated in artificial intelligence and robotics.

The market is also deeply uneven. Most new companies are valued between US$1 billion and US$2 billion, while DeepSeek and Kling AI sit far above the rest. Beijing and Shanghai lead by company count, Hangzhou leads by combined valuation, and Shenzhen has emerged as a major humanoid-robotics cluster.

The next phase will depend less on how quickly companies can raise capital and more on whether they can turn technical credibility into products, customers, revenue, and scalable operations.

H1 2026 marks a new Chinese unicorn cycle—one driven primarily by AI, embodied intelligence, and hard technology rather than consumer internet growth.