Tencent Reportedly Plans to Lead $200 Million Manus Buyback: What’s Next for the AI Agent Startup?

Tencent Leads $200 Million Manus Buyback Negotiations: What’s Next for the AI Agent Startup? Tencent reportedly leads negotiations to terminate Meta’s $2 billion acquisition of Manus. What impact could this proposed buyback have on Manus, Tencent, and the AI Agent market? Tencent Manus deal, Manus buyback, Meta acquisition of Manus

Tencent Reportedly Leads $2 Billion Manus Buyback: What’s Next for the AI Agent Startup?

Introduction

Tencent is reportedly leading negotiations that could reverse Meta’s acquisition of Manus, one of Asia’s most prominent general-purpose AI agent companies.

According to reports from the Financial Times and Reuters, Tencent is working with Manus’ management and several early investors to develop a plan to buy back the company from Meta. The proposed price is expected to be at least comparable to the original deal’s valuation of approximately $2 billion.

Negotiations are still ongoing. No final agreement has been announced, and the equity structure could change before the deal is completed.

If the current proposal moves forward, Tencent is expected to become Manus’ largest shareholder, but still a minority stakeholder. Manus would continue to operate independently rather than being integrated into Tencent.

This arrangement would elevate the transaction beyond a typical acquisition. It would be a strategic reset involving Meta, Tencent, Manus’ management, existing investors, regulators, and a product that continues to grow amid ownership uncertainty.

What Is Being Discussed?

The reported plan aims to undo Meta’s acquisition of Manus.

Meta agreed in December 2025 to acquire the Singapore-based AI startup founded by Chinese entrepreneurs. The deal was widely reported to be valued at over $2 billion, with some estimates ranging between $2 billion and $3 billion.

The acquisition later came under regulatory scrutiny in China. By April 2026, multiple reports indicated that Chinese authorities had taken steps to block or reverse the transaction.

The solution currently under discussion involves Tencent, Manus’ management, and original investors buying back the company from Meta.

Key reported terms are as follows:

| Item | Reported Position |

|---|---|

| Transaction Type | Buyback aimed at reversing Meta’s acquisition |

| Expected Price | At least $2 billion |

| Lead Investor | Tencent |

| Other Expected Participants | Manus management, ZhenFund, Sequoia Capital, and some original investors |

| Tencent’s Role | Largest shareholder, but still a minority stakeholder |

| Manus Operating Model | Expected to remain independent |

| Current Status | Negotiations ongoing; no final agreement announced |

| Future Potential Path | Continue independent growth and possibly list in Hong Kong |

This structure matters. Tencent becoming the largest shareholder does not necessarily mean Tencent will control day-to-day product decisions or directly fold Manus into one of its business units.

The minority-led structure could provide Manus with strategic support while preserving its brand, product roadmap, international operations, and ability to collaborate with partners outside Tencent’s ecosystem.

Manus’ Current Position

From Invite-Only Launch to a Major AI Agent Product

Manus gained widespread recognition in March 2025 when its early access launch generated exceptionally high demand for invitation codes.

The product was positioned as a general-purpose AI agent, not a traditional chatbot.

While conventional AI merely returns text answers, Manus can plan tasks, use browsers, write and run code, create files, analyze information, and ultimately deliver complete finished outputs.

This "execution rather than just answers" positioning helped Manus stand out in the early AI agent market.

Its product experience makes this concept easy to understand:

- Users describe the outcome they want to achieve.

- Manus breaks the request into smaller tasks.

- The agent operates within a cloud-based computer.

- It searches, calculates, creates files, and uses various tools.

- Users can view progress in real-time or let tasks run in the background.

- Manus returns a complete output for review.

Since then, the company has expanded from its initial web product into broader areas. Manus now offers web, desktop, iOS, and Android versions, along with tools for slides, websites, design, research, browser operations, email, and workflow automation.

Revenue Growth Becomes Central to the Story

Manus stated in December 2025 that its annual recurring revenue had surpassed $100 million just eight months after launch. The company also reported a total revenue run rate exceeding $125 million, including usage-based revenue.

More recent reports linked to the proposed Tencent deal suggest that by mid-2026, Manus’ recurring revenue had approached $500 million.

This newer figure is based on private company reports, not audited public financial statements. It should therefore be treated as an estimate rather than verified public documentation.

Even with this limitation, the direction is clear: Manus has evolved from a viral product launch into a commercially significant AI software company.

This commercial traction is why the current ownership talks are so important. The company now being discussed is larger and more operationally mature than the startup Meta agreed to acquire in late 2025.

Product Operations Continue

The ownership dispute has not led to a complete shutdown of Manus.

Its website remains accessible, and desktop, mobile, and cloud products continue to operate. The official website still identifies Manus as part of Meta, reflecting the legal and operational status created by the December 2025 deal.

At the same time, reports indicate that Meta and Manus have begun separating some business operations and have stopped data sharing as both sides work through the process of unwinding the transaction.

This creates an unusual transition period:

- The original acquisition was announced and implemented.

- Regulators later challenged the deal.

- The two companies have begun separating operations.

- A new investor group is negotiating a buyback.

- The product continues serving customers throughout this period.

Until a final agreement is signed and announced, users should distinguish between the product’s current public branding and the future ownership structure mentioned in reports.

Why Tencent Is Interested in Manus

Tencent has established AI agents as a core priority for both products and infrastructure.

The company is building agent products spanning office productivity, cloud services, developer tools, consumer applications, and communication ecosystems.

Specific examples include:

WorkBuddy, an intelligent AI workspace for complex office tasks.

QClaw, a lightweight AI agent environment based on the OpenClaw ecosystem.

CodeBuddy, an AI coding product from Tencent Cloud.

Agent development and governance tools within Tencent Cloud.

AI capabilities integrated with Tencent Docs, Tencent Meeting, QQ, WeCom, and related services.

Experimental agent-like features within WeChat.

This gives Tencent strong technical infrastructure, distribution channels, cloud capabilities, and a massive user ecosystem.

However, what Tencent may not yet have at a comparable scale is Manus’ experience in building a globally recognized, consumer-facing general-purpose agent product.

Product-Market Experience May Matter More Than Models

AI agent technology is increasingly sourced from multiple model providers and open-source projects.

A successful agent product still requires several layers beyond the underlying model:

- Clear user promises. Users must understand what the product can accomplish, not just what it can discuss.

- Reliable orchestration capabilities.

An agent needs to plan, invoke tools, recover from errors, and complete tasks.

3. Available interfaces. Progress, files, decisions, and failures must be visible.

4. Cloud execution. Long-duration tasks require a stable environment independent of the user's local device.

5. Cost control. Complex tasks may consume significant model and computational resources.

6. Trust and oversight. Users need to be able to inspect operations and approve critical steps.

7. Distribution channels. A powerful product still needs channels that connect individuals and enterprises.

8. Operational learning. Teams must know which tasks users actually delegate and where the agent fails.

Since its launch in 2025, Manus has accumulated experience across each of the layers mentioned above.

Therefore, for Tencent, the strategic value may not lie in acquiring a single agent architecture, but in gaining access to a team that has built, marketed, monetized, and scaled a general-purpose agent product.

Tencent's existing agent product portfolio

Tencent's AI agent strategy is already evident across several of its product lines.

WorkBuddy

WorkBuddy is positioned as an AI workspace capable of planning and completing multi-step office tasks.

Tencent states the product can support data analysis, content creation, website-related workflows, customer service, and other enterprise scenarios. It also supports parallel agents, multiple models, and remote control via services like Slack, Discord, and Telegram.

Tencent has connected it with its broader efficiency ecosystem, including Tencent Docs and Tencent Meeting.

This gives WorkBuddy an advantage in environments where users already rely on Tencent's communication, document, cloud, and enterprise tools.

QClaw and Agent Infrastructure

Tencent has also launched QClaw as a low-barrier environment for deploying and using agents.

On the enterprise side, Tencent Cloud provides infrastructure for agent development, management, monitoring, and governance. These tools aim to help organizations build agents while managing models, permissions, workflows, and production operations.

Strong product portfolio, but no global counterpart to Manus

QbitAI's monthly ranking cited in the source article shows that among the top five desktop agent products measured in June 2026, three Tencent-related products made the list, with WorkBuddy ranked first.

The chart, related to the "Strong product portfolio, but no global-class competitor to Manus" section, illustrates the market performance of Tencent-related products in the desktop agent field, indicating that Tencent has a strong product portfolio in this area.](https://we0-cms.oss-cn-beijing.aliyuncs.com/cms-assets/image/2026/07/167346d5-0cae-43c9-95d1-37c28a87e944-00279689-a2e8-460f-8387-7b5f7ffd8632.png)

{kind=link}

Such rankings depend on methodology and should not be taken as a universal measure of market share. However, they do indicate that Tencent is investing across multiple agent categories rather than relying on a single product.

Manus remains distinctive because it has become an internationally recognized agent brand before many large tech companies have launched mature general-purpose products.

This product development journey could complement Tencent's existing infrastructure and distribution advantages.

What Manus could gain from Tencent

The proposed deal could also benefit Manus.

1. Capital injection for an expensive product category

Operating a general-purpose agent is costly.

When executing a single task, it may use multiple models, long contexts, browsers, cloud computers, code execution, storage, and external tools. Rapid revenue growth does not automatically mean high profit margins.

Tencent can provide capital, cloud capabilities, model access, and procurement bargaining power, which could help Manus reduce infrastructure risk.

2. Access to enterprise-level distribution channels

Tencent serves a large number of enterprise customers through Tencent Cloud, WeCom, advertising, payments, communication, and productivity tools.

Manus could potentially reach more enterprise customers through these channels while continuing to sell its standalone product internationally.

Any integration would need to respect the company's independent operational structure and regulatory obligations.

3. Model and infrastructure support

Tencent has developed its Hunyuan (branded as Tencent Hy in some 2026 materials) model series and operates large-scale AI infrastructure.

Manus uses an agent system rather than relying on a single model. Access to more models and infrastructure can improve cost routing, latency, regional availability, and enterprise deployment options.

4. Resolution of ownership uncertainty

The current controversy has created strategic uncertainty for employees, customers, investors, and partners.

A completed share buyback could provide a clearer ownership structure and allow Manus to plan product development, financing, partnerships, and future capital market activities with fewer unresolved issues.

Why Manus might remain independent

The reported plan would make Tencent the largest minority shareholder, not the full owner.

There are several practical reasons for remaining independent.

International positioning

Manus operates from Singapore and serves users in multiple regions. An independent identity may make it easier to work with global customers and partners who do not want to rely entirely on a single large tech ecosystem.

Product neutrality

A general-purpose agent creates more value when connecting numerous models, tools, cloud platforms, and business systems.

If Manus were tightly integrated into a single company's product, it might lose some of its neutrality.

Founder and team incentives

Independent operations help maintain a startup's speed, culture, and employee incentives.

A minority shareholder structure allows a strategic investor to support the company without fully replacing the management team or product organization.

Future financing or IPO

There have been reports that Manus may form a new ownership structure with investors and eventually consider an initial public offering in Hong Kong.

This claim remains speculative. No IPO application has been filed, and no formal timeline has been announced.

However, if independence is achieved, the company would have greater flexibility to raise funds or seek an IPO in the future.

Regulatory background

The transaction between Meta and Manus is situated within broader discussions about cross-border control of AI technology, talent, data, and intellectual property.

Manus was founded by a Chinese team, subsequently moved its headquarters and operations to Singapore, and was acquired by a US technology company.

This combination raises several questions:

- Which jurisdiction has authority over the transaction?

- Where was the core technology developed?

- How should regulators handle the transfer of AI talent and intellectual property?

- What data could be shared after the acquisition?

- Would the company's relocation affect merger review?

- How should national security concerns be balanced with international investment?

Reports indicate that Chinese regulators determined the transaction needed to be unwound.

According to earlier reports, Meta has maintained that the acquisition complies with applicable laws.

The final outcome may influence how future AI startups structure cross-border financing, headquarters relocations, acquisitions, data access, and intellectual property ownership.

What might happen next?

Several possible outcomes remain.

Scenario 1: Tencent-led buyback is completed

Under the reported plan, Tencent would become the largest minority shareholder. Manus management and some original investors would also participate.

Manus would continue to operate as an independent company, while Meta would exit its ownership and financial involvement.

This is currently the primary scenario described by the Financial Times and Reuters.

Scenario 2: The investor group changes

The final investor group could include different investors or different shareholding ratios.

Some early investors may choose to exit, while new financial or strategic investors could join.

Scenario 3: Negotiations take longer than expected

An exit operation exceeding $2 billion is highly complex.

The parties may need to address the following:

- Repayment terms.

- Intellectual property separation.

- Employee arrangements.

- Existing contracts.

- Data access restrictions.

- Regulatory approvals.

- Investor rights.

- Tax and corporate structure issues.

Even if the broad direction is agreed upon, final execution may take time.

Scenario 4: Manus seeks a new financing structure

Manus could combine the buyback with new equity, debt, or a joint venture.

The report mentioned a possible future listing in Hong Kong, but this is only one potential path.

Scenario Five: No Final Agreement Reached

Negotiations may fail.

Tencent, Meta, Manus, or regulators may reject the final financial or governance structure. Until the company makes an official announcement, the deal should be considered a proposal, not a completed transaction.

What This Deal Means for the AI Agent Market

If the deal goes through, it will reinforce several trends.

Agent Products Are Becoming Strategic Assets

Big tech companies no longer view agents as small-scale experimental features.

They are investing in full-fledged products, distribution systems, cloud infrastructure, developer platforms, and acquisitions.

Commercial Execution Is Becoming More Valuable

The underlying models still matter, but product teams also need to know how to package agents into services people are willing to pay for.

Manus's reported growth rate makes its product and operational experience strategically valuable.

Independence Could Be Part of the Deal's Value

Large investors don't always need full control.

For agent platforms, maintaining neutrality and independent operations may create more value than immediately integrating into a certain ecosystem.

AI Deals Will Face More Cross-Border Scrutiny

In the future, acquisitions involving globally distributed AI companies may be reviewed based on more than just the legal jurisdiction of headquarters.

Regulators may look at the origins of founders, technology, data, funding, and strategic capabilities.

Frequently Asked Questions

Is Tencent acquiring Manus?

Tencent is reportedly leading negotiations to buy back Manus from Meta, together with Manus management and some original investors. The deal has yet to be finalized, so it's inaccurate to say Tencent has acquired the company.

How much is the proposed Manus deal worth?

Reports say the investor group plans to buy back Manus for at least $2 billion, roughly the valuation of Meta's original acquisition. Final pricing and terms have not been disclosed.

Will Tencent fully own Manus?

The reported deal structure would make Tencent the largest shareholder while remaining a minority holder. If completed, Manus is expected to continue operating independently.

Why was Meta's acquisition reversed?

Chinese regulators reportedly demanded the deal be unwound after reviewing the cross-border acquisition. The dispute involves regulatory, geopolitical, technology transfer, and ownership issues.

Is Manus still operational?

Yes. The Manus website and its cloud services, desktop version, iOS and Android products remain available. The product continues to receive updates amid ownership negotiations.

What can Manus do?

Manus is a general-purpose AI agent that plans and executes tasks in a cloud-based computer. It can research information, create files, build websites, prepare slides, write and run code, and automate workflows.

Tencent already has WorkBuddy, why does it need Manus?

Tencent already has agent technology and distribution channels, but Manus has experience building and scaling a global general-purpose agent product. Its strategic value may lie in product operations, international users, brand recognition, and monetization experience.

Will Manus list in Hong Kong?

A possible Hong Kong IPO was mentioned in reports, but Manus has not announced a formal application or timeline. It should be seen as a potential future option, not a confirmed plan.

Related Tools

Manus: General-purpose AI agent capable of research, coding, design, website building, and automation tasks.

Manus Desktop: Desktop version works with authorized local files, commands, and computer workflows.

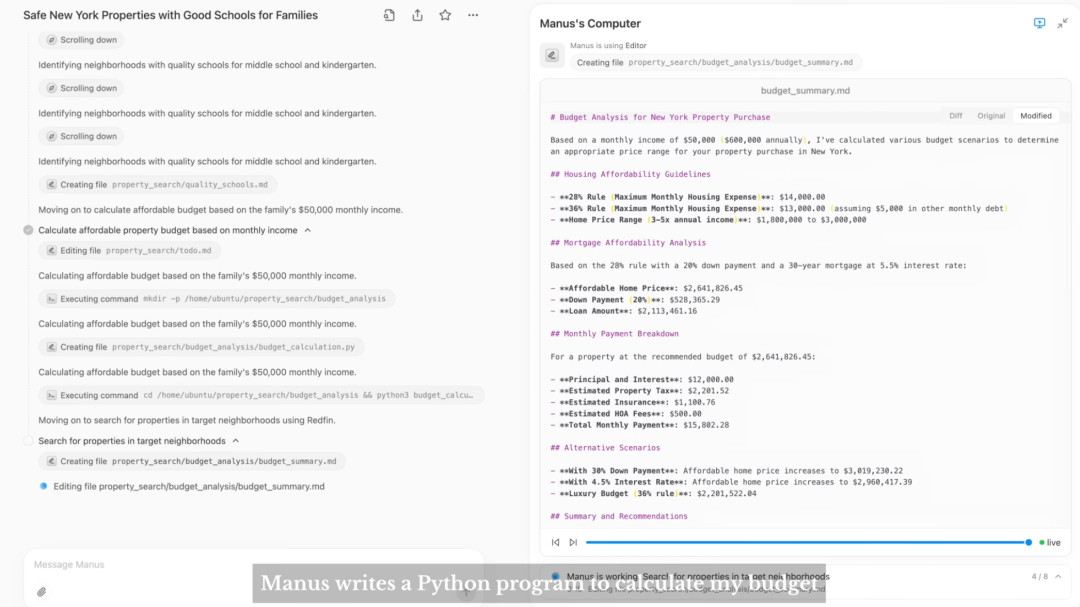

WorkBuddy: Tencent's workplace agent product for multi-step office and productivity tasks.

Tencent Cloud WorkBuddy: International version of Tencent Cloud WorkBuddy for agent deployment and business workflows.

QClaw: Lightweight environment from Tencent for deploying personal AI agents.

Tencent Cloud: Cloud infrastructure, models, and enterprise services supporting AI application deployment.

Related Links

- Reuters: Tencent in talks to become Manus's largest shareholder: Reports on Tencent-led buyback plan and current negotiation progress.

- Financial Times: Tencent-led deal unravels Meta's acquisition of Manus: Original report on Tencent's proposed role and expected equity structure.

- Manus joins Meta: Manus's December 2025 announcement regarding the Meta deal.

- Manus $100M ARR update: Official company announcement of revenue milestone in December 2025.

- Manus Documentation: Official overview of how the agent plans and executes tasks.

- Tencent launches new AI tools and enterprise solutions: Tencent's official overview of WorkBuddy and its agent strategy.

- Tencent Cloud productivity agent suite: Details on WorkBuddy Enterprise and Tencent's agent infrastructure.

- Reuters: Meta agrees to acquire Manus: Reports on the original acquisition deal and its valuation.

Summary

Tencent is reportedly leading an investment group to buy back Manus from Meta for at least $2 billion. The plan would make Tencent the largest shareholder without full ownership, allowing Manus to remain an independent company.

The deal is strategically important because Manus has built something Tencent still wants more of: a globally recognized, commercially successful general-purpose AI agent product. In return, Tencent can offer capital, infrastructure, enterprise distribution channels, and a vast product ecosystem.

The transaction is still under negotiation. Equity ratios, financing structure, regulatory requirements, and the long-term relationship with Meta have yet to be finalized.

The most accurate conclusion for now: Tencent may become Manus's most important shareholder—but Manus is expected to stay independent.